With an innovative approach to problem-solving, we recognize solutions as a driving force

- Enhance Operational Efficiency

- Designing Tailored Solutions

- Dedicated Team member

- Delivering Exceptional Value

Merchant International Bank Limited delivers secure, compliant, and scalable financial solutions to support businesses and individuals across international markets.

Years Of Experience

Merchant International Bank Limited is a global financial institution offering a comprehensive range of banking and financial services. We help businesses manage capital efficiently, navigate financial complexities, and expand confidently across international markets. Our approach is built on strong compliance standards, secure systems, and deep financial expertise.

We offer a comprehensive suite of financial tools and services designed to empower global business operations, including strategic guidance and capital solutions for mergers, acquisitions, and growth, alongside customized investment planning and asset management to protect and grow personal wealth. Our modern, tech-enabled financing solutions provide agile support for companies, while secure and flexible options facilitate global trade transactions and supply chains. We also deliver reliable international fund transfers with full RMA compliance, expert foreign exchange services with competitive rates, and a seamless payment gateway that enables businesses to manage global trade payments securely and efficiently.

Our experienced financial advisors have years of expertise providing customers with well-structured trade finance solutions. We are experts at deciphering and analysing your company's needs and then delivering services that meet those needs.

Our expert financial advisors offer professional and excellent financial suggestions to our customers to help them grow their business. For all of their banking needs, our valued customers expect nothing but the best from us, especially when it comes to essential global trade funding solutions.

Our relationship with our customers goes beyond just providing them with financial services. We at MIBL are available to our customers 24 hours a day, seven days a week. Our financial specialists are always accessible to assist you with any questions or concerns you may have, including support for essential cross-border trade funding needs.

Driving Business Forward with Trusted Strategies

Always Available, Always On, No Downtime

Stopping Problems in Their Tracks Variable

We prioritize your security and privacy by continuously updating the TF account system to deliver a safe and seamless experience, supported by advanced anti-fraud measures such as ID authentication and real-time monitoring. To maintain full protection, users should keep their information confidential, regularly review transaction history, use strong passwords, keep browsers updated, log out after each session, and avoid accessing accounts on public networks.

Individuals, Companies (LLCs, IBCs, Limited Companies), Trusts Partnerships and Foundations may all open an account with TradePAY. Accounts for entities require additional information over and above that for an individual including constitutive documents and Ultimate Beneficial Owner details traced back to a natural person. We can open accounts for almost any citizenship.

We offer an online banking platform for our clients for balance and transaction viewing and secure sending and receiving of instructions.

We provide accounts in almost all major currencies of the world like USD, Euro, GBP, AUD, SGD, NZD, CAD, HKD, CHF, CNH, INR, THB and so on.

Our business banking solutions are designed to support growth at every stage, offering tailored services such as micro financing, expert business consulting, SME loans, and corporate financing to help businesses scale strategically and efficiently.

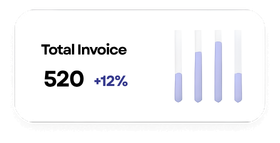

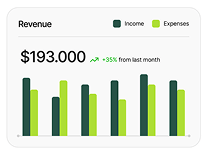

Fuel your business for long-term success with data-driven insights and performance-focused strategies. Our statistics highlight growth trends, opportunities, and key metrics, helping you make informed decisions and stay ahead in a competitive market.

Got an idea, project, or opportunity in mind? We'd love to hear from you. Reach out and let's explore how we can work together to turn your vision into something impactful and successful.

Call For Inquiry

Send Us Email

let's collaborate and create something amazing together!

15 December,2025

15 December,2025

20 December,2025

20 December,2025

31 December,2025

31 December,2025